Are you moving to Portland or relocating within the city? If you’re planning to buy a home in Portland, be prepared for stiff competition, a long search with several rejected offers, and high prices.

Portland is one of the most challenging cities for buying a house in Oregon thanks to land restrictions, high demand, and low inventory. The average home price in Portland, Oregon is about 30% over the national average and prices have increased more than 200% since 2000!

Ready for the challenge of buying a house in Portland, Oregon? Here’s everything you need to know.

Overview of the Portland Real Estate Market

The Portland housing market is one of the most expensive in the country. It’s also incredibly competitive with very little inventory. Portland housing inventory was recently below 3 weeks. In a healthy market, there is a 4- to 6-month inventory of homes for sale.

Most sellers receive multiple offers within days of listing and most homes sell above list price.

Will housing prices go down in Portland? Experts say not yet.

Portland has failed to keep up with housing starts for more than a decade. Home construction didn’t recover well from the Great Recession, and land restrictions also play a big role. A 2017 Portland law requiring new buildings with 20+ units reserve 20% as affordable housing led to many new apartment buildings with just 19 units.

Portland was ranked #3 in the country in 2017 as a good place to invest in housing development. By 2020, it had fallen to #66.

Buyers fleeing Portland’s high home prices and property taxes won’t find more affordable housing in the suburbs. Nearly all Portland suburbs are more expensive including Tigard, Beaverton, Hillsborough, and Oregon.

Average Home Price in Portland, Oregon

The Portland median home price is $550,000. That’s up from $525,000 in 2021. Portland home prices rose 17% from the median home price of $449,000 in 2020 to 2021 alone.

The average price per square foot in Portland is $342.

About 68% of homes sell above list price. The average home sells for 5.5% over list price and goes pending within 6 days.

For more context, it may help to see Portland home prices by neighborhood:

- Laurelhurst: $821,000

- Sellwood-Moreland: $720,000

- Southwest Portland: $600,000

- Northeast Portland: $625,000

- Northwest Portland: $545,000

- South Portland: $525,000

- North Portland: $511,000

- St. Johns: $460,000

What is the average home price in Portland Oregon?

- Median home price in Portland Oregon: $550,000

- Median price of a single-family home in Portland: $580,000

- Median Portland townhome price: $440,000

- Median price of Portland condos: $381,000

- Median home price in Oregon: $509,000

- U.S. median home price: $375,000

Is it Better to Rent or Buy in Portland?

Home prices have far outpaced rent in Portland. According to the 2022 Rental Affordability Report, the average weekly wage in Portland in 2021 was $1,358 or $5,432 per month. Average rent for a 3-bedroom home was $2,225 or 41% of average wages. By comparison, it would take 49% of average wages to afford the average home price of $500,000 in 2021 assuming a 3% down payment.

Another way to compare renting vs buying a house in Portland is to calculate the price-to-rent ratio. This is calculated with the median home price and the median annual rent. According to RentCafe, the average rent in Portland is $1,680.

$550,000 (Portland median home price) ÷ $20,160 (median annual rent) = 27.3 (price-to-rent ratio)

A ratio of 1 to 15 means it’s far better to buy than rent and a ratio of 21 or higher means it’s much better to rent. Portland real estate is so overpriced now, it’s much cheaper to rent than buy.

According to a recent study, the average mortgage payment in Portland Oregon was $1,141 between 2016 and 2021. The average rent during the same period was $1,485. Portland ranked #5 among cities where renters pay the lowest share of their landlord’s mortgage.

How to Buy a House in Portland, Oregon

Ready to start the process of buying a home in Portland? With the competitive Portland housing market, you’ll want to be prepared! Here are the steps you need to follow to make your dream of homeownership a reality.

Step #1: Create a Budget – How much do you need to buy a house in Portland Oregon?

To get ready to buy a house in Portland, Oregon, you need to know how much you can afford. That means it’s time to prepare an accurate budget, determine what you can realistically afford, and save up money.

Here are some tips for figuring out how much house you can afford.

Calculate Your Income

HSH.com, a mortgage data provider, found buyers would need to make a salary of $87,000 a year to buy a home in Portland. That makes Portland the 11th most expensive metro area.

While lenders will use your gross income to qualify you for a mortgage, it’s better to understand your net or after-tax income available after expenses.

List Monthly and Annual Expenses

To determine how much you can afford to spend on a house, calculate your spending on recurring monthly expenses and look for any irregular or annual expenses like car maintenance.

You may find it helpful to use budget software like Mint for this step which automatically tracks and sorts your spending and expenses.

Pay Off Debt (Optional)

If possible, it’s a good idea to pay down debt before applying for a mortgage. This will make it easier to get approved and make your mortgage payments more manageable. It can also boost your credit score to qualify you for a better interest rate which can save you thousands on your loan.

How Much Can You Afford?

Now that you know how much income you have left each month, and what you’re currently paying for housing costs, you can better assess how much home you can afford.

Lenders may advise you to buy a home around 2.5x your annual gross income, but make sure you are realistic and do not overburden yourself. Another common rule of thumb is using the 28/36 rule lenders use:

- No more than 36% of your gross income toward total debt payments (including student loans, revolving credit, car payments, etc)

- No more than 28% of your gross income toward housing costs

These are not hard and fast rules as you may not be comfortable spending this share of your income on housing. The most important thing to remember is you need to account for the total cost of owning and buying a house in Portland, Oregon.

Determine a realistic housing cost that includes:

- Principal

- Interest

- Homeowner’s insurance

- Private mortgage insurance or MIP (FHA loans)

- Property taxes

- HOA fees

Consider how much you have saved for your down payment and closing costs and how this affects what you can afford to borrow. Make sure you check below for first time home buyer programs in Portland that offer down payment assistance and more!

Portland Home Affordability Calculator

Wondering the maximum loan you can afford?

Budget for Hidden Costs of Homeownership in Portland

Remember that you need to budget for more than the mortgage payment. Here are the costs you need to consider. Average costs based on the $550,000 Portland median home price and a 10% down payment are included.

- Closing costs: 3-5% of the loan amount. Budget $15,000 to $25,000 in closing costs.

- Private mortgage insurance (PMI): Usually 0.5% to 1.5% of the loan amount per year if you put down less than 20%. Budget $2,500 to $7,500 per year.

- Homeowner’s insurance: The average Portland home insurance premium is $1,375 per year.

- Property taxes: Multnomah County property tax ranges from $13.9755 to $27.0375 per $1,000 of taxable assessed value. Check the property tax records for the home you are considering buying!

- HOA fees: If you buy a condo or a home in an HOA, your monthly HOA fees may range from $20 to more than $900 per month. The average Portland HOA fee is $450 per month.

- Utilities: The average utility bill in Portland, OR is $437 per month. Budget for higher utilities if you’re moving from an apartment to a larger home.

- Home maintenance: Budget about 1% of your home’s purchase price per year for maintenance and repairs. If you buy an older home, you may want to budget more.

Overall, the average Portland homeowner pays $12,600 per year in hidden costs of owning a home, about $2,500 more than the national average. This includes the above items plus maintenance, lawn care, and repairs.

Step #2. Get Pre-Approved for a Mortgage

With a realistic budget in mind, you’re ready to get pre-approved for a mortgage. Always get pre-approved before house hunting to ensure you are qualified for a loan and make sure your offer is viewed seriously.

To buy a house in Portland, you will generally need to meet these basic requirements:

- Down payment. Depending on the loan, it may be as low as 3-5% or up to 20%. Some loans do not require a down payment.

- Cash reserves for closing costs.

- Satisfactory credit. Most lenders require a credit score of at least 620.

- Ability to repay. Lenders usually want a debt-to-income ratio of 36% or less. Ideally, you have been with the same employer for at least one year.

- Seasoned or sourced funds. The money for your closing costs and down payment must have been in your bank account for more than 90 days. Otherwise, the lender must see the source such as a direct deposit from wages.

- Gift letter if you plan to use gifted money for your down payment.

This process is time-consuming and requires submitting a lot of documentation for your assets, income, and debts!

Make sure you check into Portland first-time buyer programs first before working with a lender – you typically need to work with an approved lender and may need to apply for the program first!

Average Down Payment in Portland

The more competitive the market, the higher average down payments tend to be. A larger down payment can strengthen your offer and significantly reduce your mortgage payment by a) lowering the principal, b) qualifying you for a lower interest rate, and c) helping you avoid private mortgage insurance (PMI).

A down payment of at least 20% is ideal, but that’s a tall order when buying a home in Portland. 20% down on the typical home would be $110,000!

Depending on your credit and the type of mortgage program, you can potentially buy a home with as little as 3% down. If you qualify for a VA loan, you can even qualify for a 0% down mortgage.

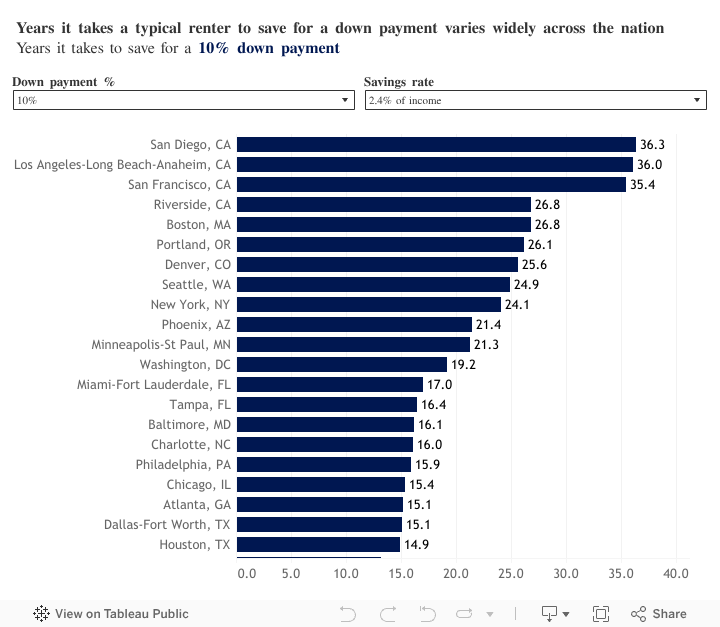

According to Zillow, the typical price for a starter home in the Portland area is $390,000, or the median in the bottom 30% of home prices in Portland, Oregon. The average renter household saving 10% of their income would need almost 13 years to save up a 20% down payment or more than 6 years for a 10% down payment.

With 10% down and a 3% interest rate, that would still be a mortgage payment of $2,320 or almost 36% of the average renter’s income.

What is the average down payment in Portland, OR? According to NAR, the average Portland home buyer puts down 14.2%. It’s one of the top 10 metros for highest median down payments.

That’s a $78,100 down payment on a median priced home ($550,000) or a $55,400 down payment on a typical Portland starter home ($390,000).

Portland First Time Home Buyer Programs

Many Portland first time home buyers are getting their down payment by taking a loan from their retirement savings, receiving funds or an advance on an inheritance from family, or requesting an early year-end work bonus.

If you are a first time buyer, you should first turn to Portland, Oregon first-time home buyer programs.

- Down Payment Assistance Loan (DPAL) from the Portland Housing Bureau offers a second mortgage of up to $100,000 at 0% interest for 30 years. Loan forgiveness begins after 15 years.

- Oregon First Time Home Buyer Savings Account lets you deduct up to $5,000 ($10,000 for couples) from your taxable income to deposit into a first time buyer savings account for up to 10 years.

- HomeStart Down Payment & Closing Cost Assistance from FHLB Des Moines offers up to $7,500 in forgivable closing cost and down payment assistance.

- Portland Housing Center offers Individual Development Accounts (IDAs) with savings matched 5:1 and a Mortgage Assistance Program with up to $80,000 in down payment assistance to eliminate PMI or FHA mortgage insurance.

- Hacienda Community Development offers 3:1 matched savings plans and down payment assistance loans.

- Proud Ground offers affordable Portland, Oregon homes for sale through Community Land Trusts (CLTs)

- DevNW offers up to $15,000 in down payment assistance for lower income first time buyers.

- Oregon Bond Residential Loan Program offers below-market interest rates on first time home buyer mortgages or loans with 3% cash closing cost assistance.

- Oregon Veteran Home Loan is a state veteran’s mortgage with no funding fee and low interest rates.

Read our complete guide to Oregon first time home buyer programs for more information!

Step #3. Hire a Real Estate Agent in Portland

After pre-approval, the next step is choosing a buyer’s agent to help with buying a house in Portland. Your agent will guide you through the process, help you explore neighborhoods, show you homes, protect your best interests, and assist with putting in offers and negotiating.

A good real estate agent responds quickly to your communications and seems to have enough time for you. You should feel comfortable in their knowledge, skill, and experience. Look for an agent with experience in your price range and the areas of Portland high on your list.

Step #4. Start House Hunting in Portland!

Now you’re finally ready for the exciting part of buying a home in Portland, Oregon: house hunting! Your real estate agent will help you explore neighborhoods in Portland or the Portland suburbs that fit your budget and what you’re looking for.

It’s important to stay realistic about your expectations. Focus on your needs and deal-breakers and remember the things you can’t change – like the location and school district – are more important than cosmetic things you can change later.

Here are some things to think about while exploring Portland, Oregon real estate.

- Location

- Home type & age

- HOA fees

- Commute

- School district

- Property tax rates

- Crime

- Distance to highways and public transportation

- Walkability

- Traffic and overall neighborhood noise

- How well-kept homes are in the neighborhood

- Nearby amenities

You can start your search online for Portland, OR real estate to explore areas and get an idea of what to expect.

Step #5. Submit an Offer

Once you find a home that fits your needs, be prepared to move fast! The Portland housing market is very competitive with homes going pending in just 6 median days, selling for over listing, and receiving multiple offers.

Your real estate agent will give you advice for crafting the strongest offer possible. You may increase your odds of getting your offer approved by reducing contingencies, making the offer as-is contingent on an inspection, or coming in at your best price from the start.

Don’t be discouraged if your offer isn’t accepted. An Opendoor report in 2021 found the average first time home buyer made 5 or more offers before one was accepted and toured 15 properties. In very competitive markets like Portland, rejection is practically guaranteed.

Step #6. Close on Your New Home!

When you finally get an accepted offer, you will be under contract. Over the course of the next month or two, there will be plenty of paperwork to complete. You will need to complete underwriting to secure your mortgage and sign off on the home inspection. Once all contingencies are met, closing will be scheduled. After you sign a stack of paperwork and do a final walkthrough, you will close on your home and be ready to move in!

Are you preparing for the daunting task of buying a house in Portland, Oregon? The home buying process is stressful enough, moving into your new home shouldn’t be! Call PDX Movers for a free, personalized estimate from our experienced Portland movers. We’ll coordinate your move so you can start enjoying everything homeownership has to offer.